African Food Market Analysis Report 2025 to 2030. Market Size, Growth Forecast, Trade Corridors, Investment Hotspots, and Innovation

Executive summary

Africa's food market generated $865.9 billion in revenue in 2025 and is tracking toward $1.25 trillion by 2029, a 9.66% compound annual growth rate (Statista). Meat alone accounts for $163.2 billion of that, the largest single segment.

Behind the numbers sits a continent of 1.4 billion people, with agriculture making up about 35% of GDP and employing roughly half the workforce (World Economic Forum). The continent still imports billions of dollars of food every year while shipping some of the world's most sought-after raw commodities abroad.

That gap between what Africa grows, what it eats, and what its trading partners need is where value moves. This report maps it. You get the market size, the commodities driving export revenue, the corridors carrying African goods to the Gulf and Europe, the countries worth an investor's attention, and the technology changing how food travels from a smallholder plot to a port.

What this report covers

The full analysis runs across market sizing and forecasts, product and regional segmentation, supply and demand fundamentals, a trade corridor breakdown, commodity price movement, the regulatory and sustainability landscape, the countries holding the biggest investor potential, and the innovation wave now reshaping the sector.

Market context and demand fundamentals

Three forces set the direction.

Population. Africa's population is projected to reach 2.5 billion by 2050, most of it urban. City dwellers buy food rather than grow it. That single shift converts subsistence farming into commercial demand at scale.

Income. A growing middle class is spending more on protein, packaged goods, and branded products. The Africa food and beverage market was valued at $346.23 billion in 2024 and is forecast to reach $567.31 billion by 2032 at a 6.34% CAGR (Verified Market Research). Beverages and organic subsegments are climbing faster than the average, with organic projected above 12% CAGR in key urban areas.

Trade policy. The African Continental Free Trade Area (AfCFTA) is the structural change underneath all of this. It covers a market projected to host 1.7 billion people and $6.7 trillion in consumer and business spending by 2030 (World Economic Forum).

Market size and growth forecast

The headline figure of $865.9 billion in 2025 rising to $1.25 trillion by 2029 describes consumption inside Africa. The export economy runs alongside it.

African agricultural exports grew by more than 20% between 2020 and 2024, pulled by demand for natural oils, spices, and wellness crops (FAO, Trade.gov data cited by trade sources). The African Development Bank's African Economic Outlook 2026 found that agriculture and industry were the main drivers of the continent's growth in 2025, with agriculture contributing 0.9 percentage points to overall GDP growth.

Segmentation by commodity and region

Export revenue concentrates in a handful of commodities, and each has a clear origin map spread across several countries.

Coffee. Ethiopia's coffee sector generated $351 million in Q1 2026 exports, close to two-thirds of the country's agricultural export earnings (Ministry of Trade and Regional Integration). Uganda's coffee brought in $181 million in the same quarter. Ethiopia, Kenya, and Uganda anchor African specialty coffee.

Cashew. Tanzania emerged as Africa's leading cashew exporter at $560 million in Q1 2026. Nigeria, Ivory Coast, and Guinea-Bissau round out the top suppliers. Value addition through shelling and roasting raises margins meaningfully, and processing capacity is expanding across origins.

Sesame. Ethiopia, Sudan, and Nigeria lead. In 2025, more than 80% of sesame imports at specific Chinese ports came from Africa, helped by zero-tariff treatment (China Daily). Nigeria's sesame exports were valued at ₦247.75 billion in Q1 2024 (Nigeria's National Bureau of Statistics).

Oilseeds and vegetable fats. These are among the fastest-growing export groups. Oilseeds and oleaginous fruits recorded roughly 14% to 15% growth, and animal and vegetable fats such as shea butter grew 16% to 17%.

Pulses. Ethiopia and Tanzania export high-quality pulses into steady global demand from plant-based diets. Tanzania alone accounts for 4% of the world's pigeon pea production.

Supply-side reality

Africa holds the largest share of the world's land suitable for sustainable production expansion (African Leadership Magazine). The constraint is rarely land. It is everything between the farm and the buyer.

Smallholders produce more than 80% of the African food system (Climate Resilient Africa Fund). Post-harvest loss, weak storage, thin logistics, and limited port capacity strip value before goods ever reach a ship. Only about 30% of African farms have reliable internet access, which slows the data-driven tools that could close yield and quality gaps.

Direct sourcing changes the arithmetic here. Every intermediary layer between a farming region and a buyer adds cost and blurs traceability. Operators working directly with farming cooperatives, which is the model ASAFI built its Africa sourcing around, hold tighter control over quality, price, and the paper trail buyers increasingly demand.

Demand-side pull

Two external buyers matter most for African exporters.

The Gulf. The Gulf Cooperation Council imports about 85% of its food and consumes roughly $29.5 billion worth each year (World Economic Forum). Desert geography, water scarcity, and limited arable land make heavy domestic production unrealistic for most staples. GCC governments have committed $3.8 billion to agri-tech and identified a $30.5 billion food-security opportunity, yet the underlying import dependence remains. That structural need is a durable demand signal for African origins that can supply reliably. ASAFI's own analysis of GCC food security lays out how thin the region's margin for supply disruption actually runs.

Europe. The European Union is a mature, high-value destination for coffee, cocoa, nuts, and fruit. It also sets the strictest standards, which raises the bar and the reward for compliant suppliers.

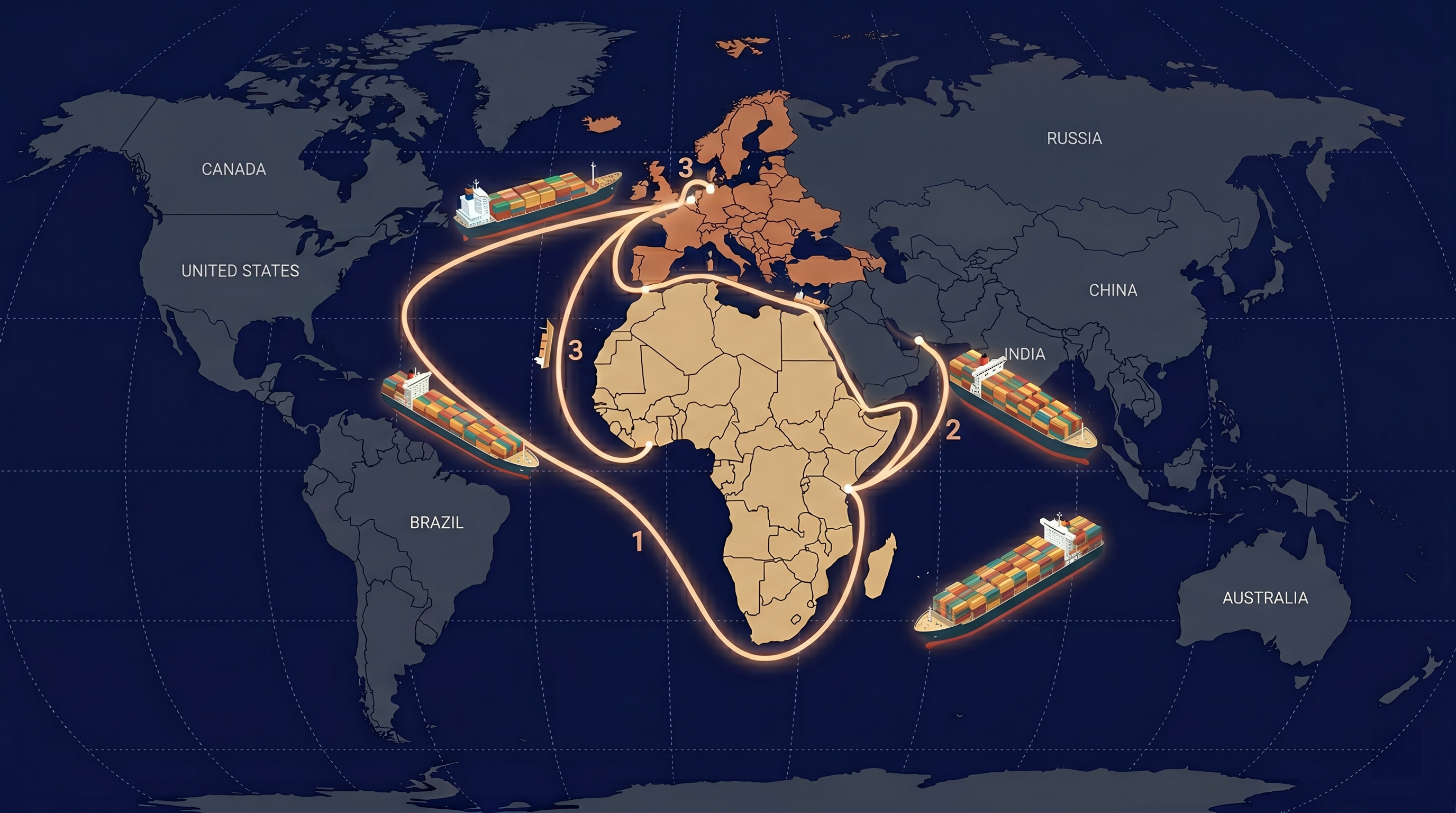

Trade corridor deep dive

Africa's internal trade is still surprisingly small. Only about 14.8% of Africa's trade is internal, against 54.5% for Asia and 68.4% for Europe (ISS African Futures). Most African goods head outward, to the Gulf, Europe, and increasingly Asia.

AfCFTA is built to change that balance. If import tariffs are eliminated, intra-African agricultural trade is projected to rise by 574% by 2030 (World Economic Forum). The Economic Commission for Africa estimates that full implementation could lift intra-African trade by 45%, worth $275.7 billion, with agri-business set to benefit the most among all sectors.

The friction is real. High tariffs, slow customs, and patchy infrastructure keep costs elevated. For buyers, the corridors that already work, the direct farm-to-Gulf and farm-to-Europe routes, carry a reliability premium that the fragmented multi-hop chains cannot match.

Commodity price analysis

Price behavior in 2025 and 2026 rewarded diversified sourcing.

Coffee. Arabica futures hit a historic high of $4.41 per pound in February 2025 and peaked again near $3.80 in January 2026 (ICE data via trade sources). Certified arabica stocks sat well below historical averages. Brazil, which grows roughly a third of the world's coffee, is heading for a record 2026/27 harvest estimated at 66 to 75 million bags, yet prices stayed above $3 per pound through mid-2026 because stocks were thin and Brazil's harvest ran behind pace. When your roasting volume leans on one or two origins, any shock in either moves your whole cost base. Buyers spread across smaller African origins absorbed less of that swing.

Cashew, sesame, and pulses held firmer demand from Asia and the Middle East, aided by China's preferential tariff treatment for several African-origin products.

Regulatory and sustainability landscape

The rules tightened, then bent.

The EU Deforestation Regulation (EUDR) requires proof that covered goods, including coffee, cocoa, cattle, palm oil, rubber, soy, and wood, are free from deforestation after 31 December 2020, backed by farm-level geolocation data. After repeated delays, the application date for large and medium operators now lands on 30 December 2026, with micro and small operators following in June 2027 (European Council). A simplification review is due by 30 April 2026.

The direction of travel points one way. Traceability from the specific plot of land becomes the price of entry to premium markets. Suppliers already collecting that data at origin gain a head start. Gulf import standards and halal certification add a parallel compliance layer, making verified, documented supply chains a competitive asset rather than a cost.

Which African countries hold the biggest potential for investors

Opportunity is uneven. Seven markets stand out on production scale, infrastructure, and buyer access.

Nigeria. The largest agricultural market on the continent at roughly $60 billion, with agriculture at 24% of GDP and 40% of national export earnings. Non-oil exports climbed to ₦12.36 trillion in 2025, up from ₦9.09 trillion in 2024. Cocoa, sesame, and cashew lead the export mix. A population of 228 million gives it enormous domestic demand alongside export volume.

Ethiopia. Agriculture accounts for 36% of GDP. Coffee is the top foreign-exchange earner, backed by sesame, pulses, oilseeds, and cereals. For buyers seeking specialty green coffee and quality oilseeds at origin, Ethiopia is a primary source.

South Africa. The most mechanized and infrastructure-rich agricultural market, valued at over $30 billion, with more than 40,000 commercial farmers and the continent's most developed supply chains and ports. It is also the continent's digital-agriculture frontrunner.

Kenya. The clearest agtech leader. It secured $63 million in agri-tech funding in the first half of 2024, a 62% year-on-year jump (Briter). With a $108 billion GDP and strong tea, coffee, avocado, and flower exports, it functions as the East African hub for investors.

Egypt. Agriculture contributes 14% of GDP and 20% of export earnings, supported by modern irrigation, vertical farming, and greenhouses. A $396 billion economy and 114 million people make it a scale market in North Africa.

Tanzania. Africa's top cashew exporter at $560 million in early 2026, with growing pulse and pigeon pea volumes and expanding processing ambitions.

Morocco. An agricultural market of around $25 billion, roughly 15% of GDP, with heavy state investment and strong access to European markets.

The immense potential for growth and innovation

The technology story carries a twist worth understanding before you read the funding numbers.

African agtech funding fell to under $170 million in 2025, down nearly 20% from over $200 million in 2024 (State of Agtech Investment in Africa 2025). Equity funding dropped from roughly $328 million in 2022 to about $80 million in 2025. Read alone, that looks like retreat.

The full picture is different. The money did not vanish. It changed shape. Debt overtook equity for the first time, and blended finance now carries the scale-up work that venture capital used to fund. Agtech in Africa is asset-heavy. It runs across logistics, input distribution, aggregation, and farmer financing, which needs working capital and longer payback than a software startup. The shift toward debt and blended finance signals a maturing ecosystem moving toward capital-efficient, infrastructure-driven models.

The upside is large and specific. Agri-tech innovations are projected to boost farm yields by up to 30% through AI-powered precision tools, climate-smart practices, and digital finance (multiple 2025 sources). South Africa is on track for 60% of its farmers adopting digital agri-tech solutions by 2025. Kenya, Egypt, and Nigeria concentrate most of the continent's best-funded startups.

The AKADEMIYA2063 Annual Trends and Outlook Report 2025 delivers the sharpest finding. Africa already has the innovations it needs. The bottleneck is integration, governance, financing, and adoption, not invention. The CAADP 2026-2035 Strategy aims to mobilize $100 billion in public and private investment to close that gap.

The categories drawing the most capital tell you where the durable value sits. Ag marketplaces, fintech, and midstream technologies lead, because they penetrate the smallholder base that runs 80% of the food system. Supply-chain orchestration, soil-health data, and traceability round out the priority list. These are the exact capabilities the EUDR and Gulf import standards will soon require, which turns compliance pressure into an investment thesis.

Forecast scenarios to 2030

Base case. Consumption follows the 9.66% CAGR toward $1.25 trillion by 2029 and beyond. AfCFTA implementation proceeds unevenly. Export commodities hold firm demand from the Gulf, Europe, and Asia. Direct-sourcing operators with traceability capacity take share from fragmented chains.

Upside case. AfCFTA tariff elimination accelerates, pushing intra-African agricultural trade toward the projected 574% increase by 2030. Blended finance unlocks midstream infrastructure. Yield gains near the 30% ceiling in leading markets.

Downside case. Climate volatility, currency instability, and regulatory uncertainty around EUDR timelines slow investment and disrupt supply. Post-harvest loss and logistics gaps continue to strip value.

The variables that move the outcome most are climate resilience, infrastructure investment, and the pace of AfCFTA and traceability adoption.

Strategic implications

For sourcing operators, the durable margin sits in direct origin relationships, quality control at the farm gate, and traceability data collected before buyers ask for it.

For Gulf and European buyers, supply security now depends on diversified origins and documented chains. A single-origin strategy carries price and compliance risk that spreads across the whole book when one region stumbles.

For investors, the money is following infrastructure and data, marketplaces, midstream technology, and traceability, the capabilities that make African supply reliable enough to command premium prices.

The continent that feeds the world has spent decades struggling to feed itself. The next five years decide whether it starts doing both.